Mr. Ramesh Vaghasia

Chairman, Axanoun Investment Services

Introduction

A semiconductor is a material whose electrical conductivity lies between metals (like copper) and insulators (like glass). Its key advantage is controllable conductivity— electricity can be allowed or restricted as needed. This property underpins modern electronics, including smartphones, computers, automobiles, telecom systems, and data centers. Semiconductor manufacturing starts with a purified silicon wafer. The material is modified to control electricity, forming microscopic switches. Multiple circuit layers are built through repeated precision processes. The wafer is then cut into individual chips, which are packaged, connected, tested, and supplied to electronics manufacturers. Semiconductors are critical to modern electronics, with demand driven by three areas: data centres (AI and high-performance computing), automobiles (especially EV power and driver systems), and connectivity (5G and Internet of Things devices).

The Rise of a Trillion-Dollar Industry

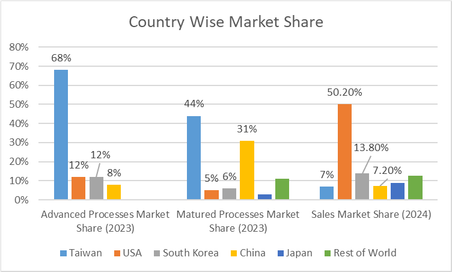

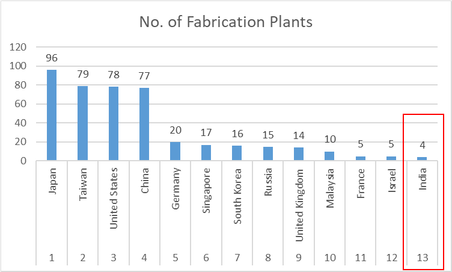

One of the earliest semiconductor applications was the “cat’s whisker” detector developed in the early 1900s by Jagadish Chandra Bose for radio signal detection. The industry later expanded in Silicon Valley after Fairchild Semiconductor was founded in 1957, leading to companies such as Intel and AMD. Growth accelerated under Moore’s Law, which predicted improving chip performance alongside declining costs. Since its early innovations, the semiconductor industry has become a global economic pillar, with a market size of approximately US$600– 700 billion in early 2025, projected to reach nearly US$1 trillion by 2030, driven by artificial intelligence, cloud computing, and data center expansion. The chart highlights geographic concentration in semiconductors: Taiwan holds 68% of advanced manufacturing and 44% of mature processes, while China has 31% of mature production. The United States leads global semiconductor sales with a 50.20% share. 7 Chips, AI and EVs The Management Memo Fabrication data shows Japan has the most semiconductor plants globally, followed by Taiwan, the United States, China, and Germany. These five countries together account for nearly 75% of global fabrication capacity.

At the company level, TSMC leads semiconductor manufacturing with 55–60% global foundry share and over 70% of advanced chip production. It manufactures chips for major firms such as NVIDIA, Apple, AMD, and Qualcomm, and is the primary producer of advanced AI and high performance computing chips. Among other leaders, NVIDIA is the world’s largest semiconductor company by market value, driven by AI chip design. Samsung holds around 15% foundry market share, while Intel remains a major integrated chip manufacturer. Broadcom focuses on networking, broadband, and infrastructure semiconductor solutions. The Rise of a Trillion-Dollar Industry One of the earliest semiconductor applications was the “cat’s whisker” detector developed in the early 1900s by Jagadish Chandra Bose for radio signal detection. The industry later expanded in Silicon Valley after Fairchild Semiconductor was founded in 1957, leading to companies such as Intel and AMD. Growth accelerated under Moore’s Law, which predicted improving chip performance alongside declining costs.

Since its early innovations, the semiconductor industry has become a global economic pillar, with a market size of approximately US$600– 700 billion in early 2025, projected to reach nearly US$1 trillion by 2030, driven by artificial intelligence, cloud computing, and data centre expansion. The chart highlights geographic concentration in semiconductors: Taiwan holds 68% of advanced manufacturing and 44% of mature processes, while China has 31% of mature production. The United States leads global semiconductor sales with a 50.20% share. 7 Chips, AI and EVs The Management Memo Fabrication data shows Japan has the most semiconductor plants globally, followed by Taiwan, the United States, China, and Germany.

These five countries together account for nearly 75% of global fabrication capacity. At the company level, TSMC leads semiconductor manufacturing with 55–60% global foundry share and over 70% of advanced chip production. It manufactures chips for major firms such as NVIDIA, Apple, AMD, and Qualcomm, and is the primary producer of advanced AI and high performance computing chips. Among other leaders, NVIDIA is the world’s largest semiconductor company by market value, driven by AI chip design. Samsung holds around 15% foundry market share, while Intel remains a major integrated chip manufacturer. Broadcom focuses on networking, broadband, and infrastructure semiconductor solutions.

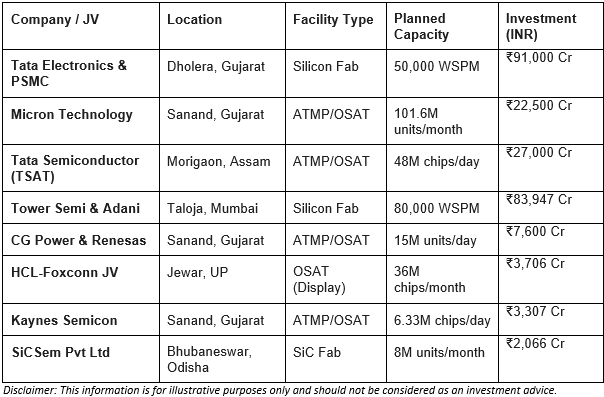

India’s Semiconductor Ecosystem

History, Policy Push, and Emerging Industry Players

India’s semiconductor journey began in the 1960s with Bharat Electronics, followed by SCL Mohali in 1983. By the mid-1980s, India was near global standards. A 1989 fire destroyed the Mohali facility, and later delays and regulatory hurdles led to missed opportunities, with investments shifting to China and Malaysia. India imports 90–95% of its semiconductor needs, worth ~US$18 billion annually, mainly from Taiwan, China, South Korea, and Singapore. To reduce dependence, the government launched the India Semiconductor Mission (ISM) in 2021 with a ₹76,000 crore package, offering up to 50% support for fabrication and display units, along with incentives for chip design firms. ISM 2.0 expands support to materials, equipment manufacturing, and IP development to build a full ecosystem. India’s semiconductor push is cantered in Gujarat, with Dholera focused on large-scale fabrication and Sanand on assembly, testing, and packaging. Together, they form the core of India’s semiconductor manufacturing ecosystem.

Major Indian companies foraying into this segment are as follows:

Conclusion

The semiconductor industry is set for strong growth, driven by AI, electric vehicles, and the Internet of Things. The India Semiconductor Mission can accelerate domestic manufacturing and strengthen India’s position in the global value chain. However, risks remain significant. A large portion of the global supply chain is concentrated in Taiwan, and any adverse geopolitical developments could disrupt supplies, leading to shortages and affecting a wide range of dependent industries.